COTCollector Wealth-Lab Static Data Adapter

The COTCollector Static Data Adapter for Wealth-Lab allows direct access

to Commitments of Traders data stored in COTCollector from within Wealth-Lab.

You can create one or more COTCollector datasources which are automatically updated

when you update COTCollector (or when the scheduled weekly update runs).

Updated for COTCollector 3.05

Updated for COTCollector 3.05

Click here for the Wealth-Lab 5.x COTCollector DataSet Provider

Download the COTCollector 3.0 Static Data Adapter

for Wealth-Lab Pro 3.x/4.x (394 KB)

Download the COTCollector Static Data Adapter for Wealth-Lab Developer 3.x/4.x (394 KB)

Note: You must install COTCollector (available from the

Downloads link above) before

using the static data adapters.

Installation

First install COTCollector, then install the appropriate static data adapter for

Wealth-Lab. The installation should automatically detect the location of your

Wealth-Lab folder, but please verify the target folder during the install (like

all static data adapters for Wealth-Lab, the COTCollector static data adapter must

be installed to the same folder as Wealth-Lab).

Usage

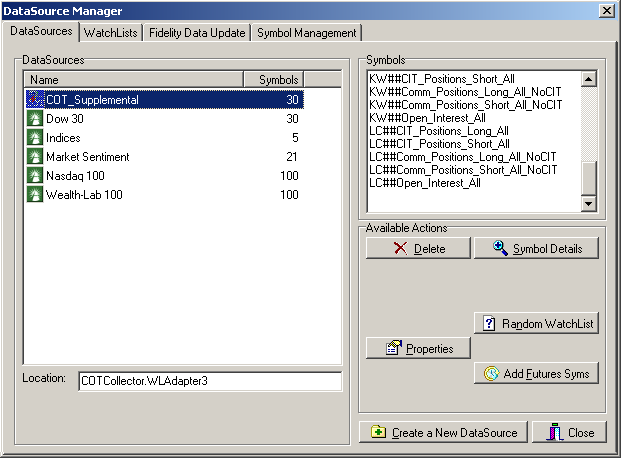

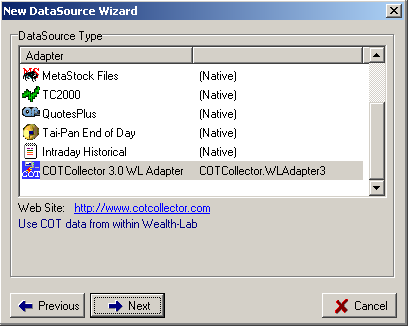

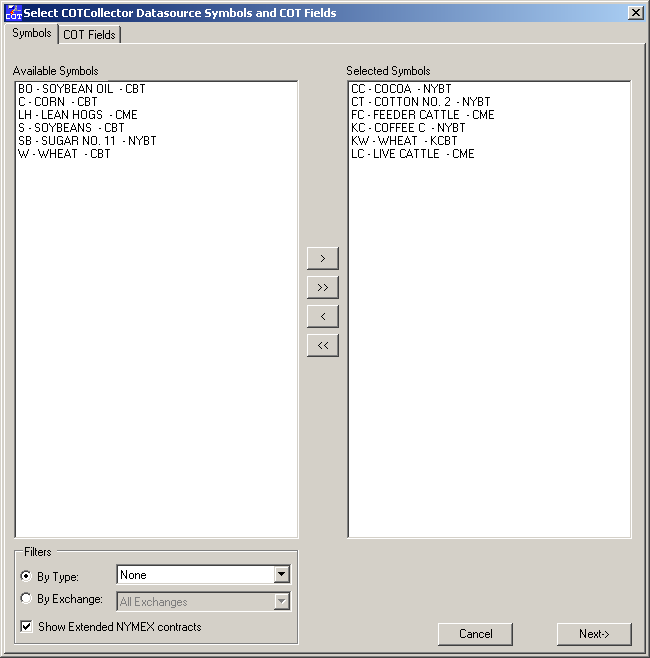

From within Wealth-Lab, click "Data Sources" and then "Create a New Datasource".

Then scroll to the bottom of the list and choose COTCollector WL Adapter.

Click Next to continue. This will launch the COTCollector Datasource Selection

Dialog. Select all the symbols you want in the datasource and click Next.

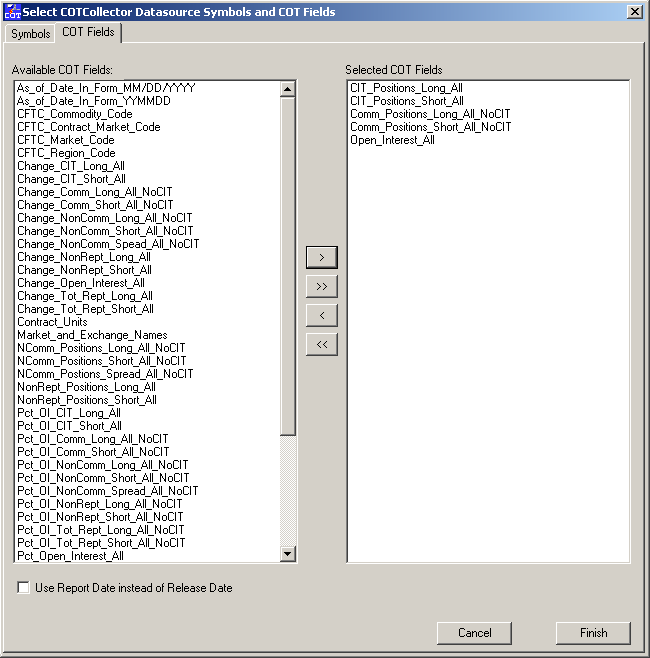

Select the COT Fields you want in your datasource and click Finish to create the

datasource. You can select from pre-defined COT fields or the aliases you've

defined for them. Check "Use Report Date instead of Release Date" to retrieve

data based on the date is was collected, not reported. Generally COT data

is collected on Tuesday and released on Friday so choosing this will make the data

available as of that Tuesday, essentially peeking into the future. However

this can be useful to view the data side by side with prices.

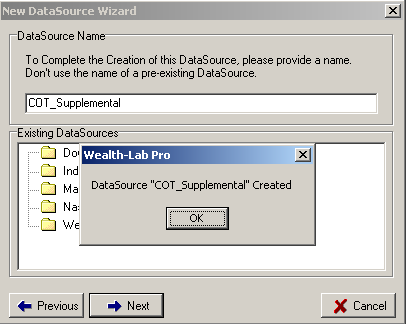

Finally, choose a name for your data source and click Next to create the datasource

in Wealth-Lab.

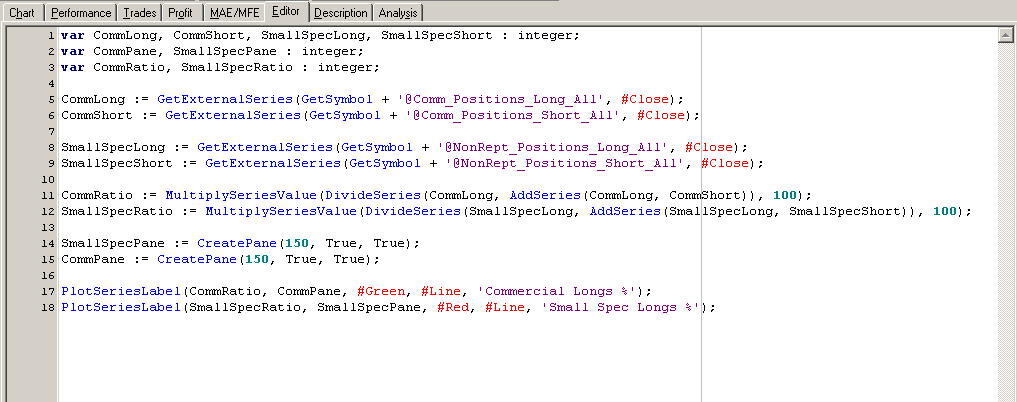

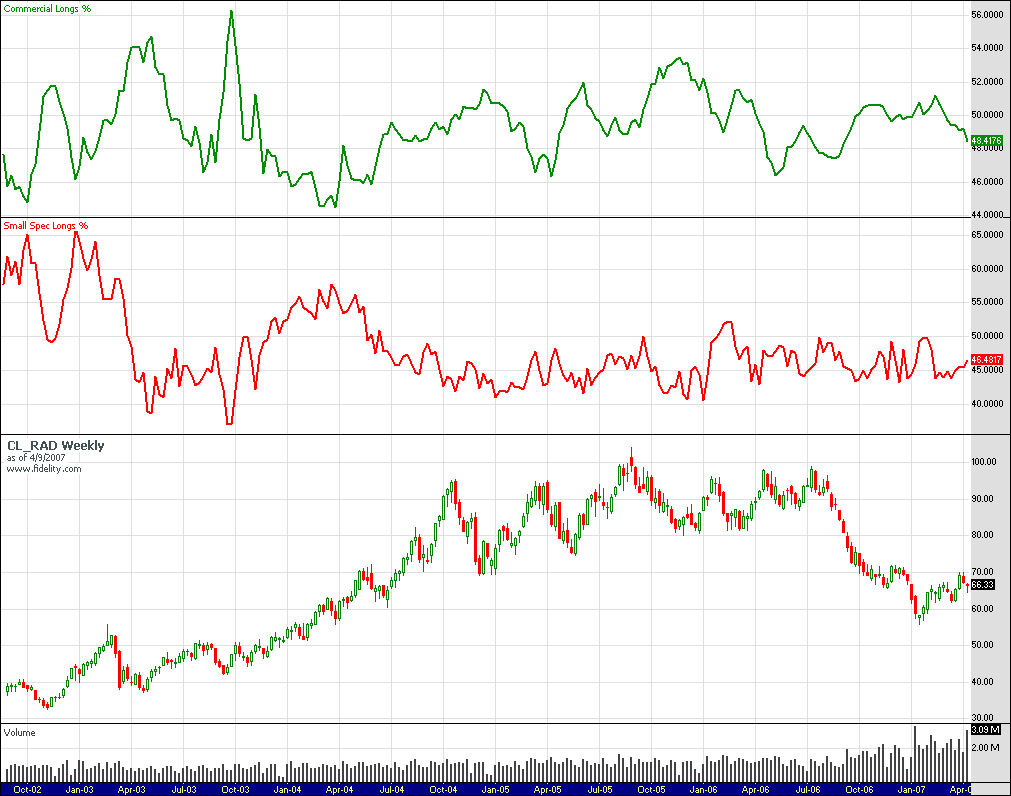

You can then use COT data directly within scripts. Reference each symbol in

the format [Symbol]##[COTField]. For example CL_RAD##Comm_Positions_Long_All

or CL_RAD##CL (if you defined CL as an alias for Comm_Positions_Long_All).